Cost per Unit (Manufacturing) Sensitivity Analysis Financial Excel Model

![Cost per Unit (Manufacturing) Sensitivity Analysis Financial Excel Model - Templarket - Business Templates Marketplace]()

Cost per Unit (Manufacturing) Sensitivity Analysis Financial Excel Model

Available:

In Stock

$45.00

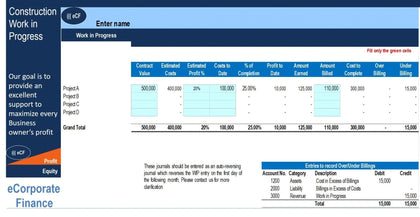

This quantitative financial tool comes with a primary cost per unit scenario analysis and a set of charts to visualize the results. Two other identical tabs are included for multiple strategy tests.

The way it works is really simple. You enter all your costs for a given period. Then, simply enter 3 levels of sales volume amounts and your desired profit margin %.

Based on the entered assumptions, the tool will tell you what the selling price should be in order to achieve your desired profit margin for a given level of sales volume.

The key here is seeing what kinds of price points might make sense in different possible scenarios.

The main costs you will enter include:

1. Supplies and materials

2. Multiple types of labor along with their head counts

3. Sales & Marketing (advertising, salesmen, other)

4. Overhead such as Rent, Legal, and other)

You will notice that as you raise the total sales volume for the period being measured, the required sale price per unit will go down as well as the cost per unit. This is because you are solving for a pre-defined profit margin and holding that value constant means lower price points in order to make the same margin, or you could raise the margin so that the price point stays the same, but you total profit goes up.

There are many uses that come into play with such a cost per unit model.

The way it works is really simple. You enter all your costs for a given period. Then, simply enter 3 levels of sales volume amounts and your desired profit margin %.

Based on the entered assumptions, the tool will tell you what the selling price should be in order to achieve your desired profit margin for a given level of sales volume.

The key here is seeing what kinds of price points might make sense in different possible scenarios.

The main costs you will enter include:

1. Supplies and materials

2. Multiple types of labor along with their head counts

3. Sales & Marketing (advertising, salesmen, other)

4. Overhead such as Rent, Legal, and other)

You will notice that as you raise the total sales volume for the period being measured, the required sale price per unit will go down as well as the cost per unit. This is because you are solving for a pre-defined profit margin and holding that value constant means lower price points in order to make the same margin, or you could raise the margin so that the price point stays the same, but you total profit goes up.

There are many uses that come into play with such a cost per unit model.